To the overview of the basics

→ To the home page

Is crypto safer than banks?

This is a question that comes up a lot: Is cryptocurrency actually safer than a bank account?

The short answer is: It’s not that simple to say.

Banks and blockchain systems are essentially trying to solve the same problem—making money usable while keeping it secure. The only difference lies in how this security is organized.

In the banking sector, this is achieved through rules, institutions, and infrastructure.

In blockchain systems, however, it is achieved through the possession of a digital key.

Both approaches work—but in completely different ways. That’s exactly the difference we’ll be taking a closer look at on this page.

Table of Contents

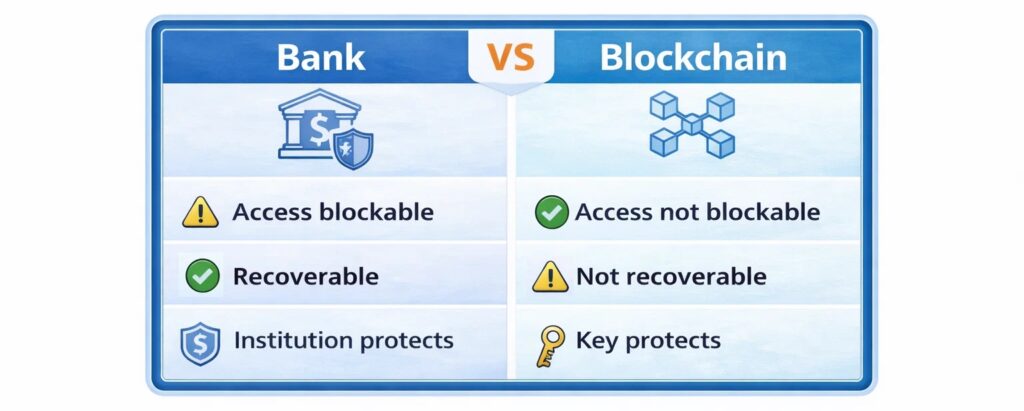

Two security models

Ultimately, both banks and blockchain systems are striving to achieve the same goal: money should be secure while also being easy to use in everyday life. The only difference lies in how this security is organized.

In the banking sector, this is primarily based on administrative processes. A financial institution manages the account, monitors transactions, and can intervene or restore access in an emergency.

Blockchain systems work differently. Here, possession of a digital key determines whether someone can move funds or not.

This means that it is not the money itself that is organized differently—but control over it.

How banks create security

When you use a bank account, there is always a managed system running in the background.

You log in using your credentials, the bank manages your account, and ensures that payments are processed. This is convenient for everyday life because so much happens automatically.

If you forget your password or something goes wrong, access can be restored. At the same time, however, this also means that all usage always goes through the bank’s infrastructure.

In other words: The bank provides access and ensures that the system works.

As long as everything runs smoothly, you hardly notice it. It’s only when payments are flagged, systems go down, or processes are interrupted that it becomes clear that access is managed by an institution and you have no direct control over it.

How blockchain creates security

Security in blockchain systems works fundamentally differently than in banks. There is no institution here that maintains an account or approves transactions. Instead, possession of a digital key determines whether someone can move funds or not. This key belongs solely to the user. Whoever possesses it can execute transactions—whoever does not have it cannot make any changes.

This also means that there is no central authority that can restore access or stop payments.

Security, therefore, does not come from administration, but from direct possession of the key.

This shifts the responsibility: it is not an institution that protects access, but the user themselves.

What may be canceled in each case

The differences between banks and blockchain usually only become apparent when something doesn’t work as usual.

With a bank account, for example, access may be temporarily restricted—due to audits, technical issues, or regulatory requirements. The funds themselves do not disappear, but access to them may be temporarily suspended. However, there are usually ways to restore access.

With blockchain systems, the situation is exactly the opposite. There is no institution that manages access. Anyone who possesses the private key can use the funds. However, if this key is lost or not properly secured, there is usually no central authority that can restore access.

So both systems aim to make money safe—just in different ways.

Banks ensure security through organization and recovery.

Blockchain through direct ownership and control.

The key difference, then, is not which system is “perfect”—but where responsibility lies.

When this becomes relevant in everyday life

In everyday life, the two feel almost the same. You pay with a card, transfer money, or use an app—and everything works seamlessly. The difference only becomes apparent when things no longer run automatically.

For example, when

- an account is being verified

- a system is temporarily paused

- technical issues may arise

- or there is no access to a key

In situations like these, you suddenly realize that there is always a structure standing between money and its use. That’s when it becomes clear who actually has the power to decide whether a transaction goes through or not. And this is precisely where the real difference between the two systems lies:

It’s less about technology—and more about where control and responsibility lie.

It is precisely at this point that many people begin to question how their own access to money is actually organized.

It is also worth taking a look at the legal basis for bank deposits.

Why more and more people are asking themselves this question

As long as everything runs smoothly in everyday life, most people hardly ever think about how their money is actually managed. Transfers go through, cards work, payments are processed—and the system seems to just work.

It’s only when you take a closer look that you realize there’s a structure behind every payment that manages access.

That is precisely why more and more people today are interested in how monetary systems actually work and what alternatives exist to the traditional banking model. For most people, the goal is not to completely replace banks. Rather, it is about gaining a new perspective: understanding where control lies and what alternatives are available.

Conclusion

Banks and blockchain follow two completely different security principles:

Banks give you permission to use their services.

Deobank gives you control.

One protects you better against your own mistakes.

The other protects you better against unauthorized access.

Which structure makes more sense therefore depends less on the technology—and more on how much responsibility you want to take on yourself.

If you’d like, we can take a look at how your own access to funds is currently organized.

Ultimately, this is less a technical question than a personal one: How would you like to manage access to your money in the future?

FAQ – Comparison of banks and blockchain

Is crypto safer than a bank account?

Both systems protect money in different ways: banks through administration and recovery, blockchain through direct control of a key.

Who controls access to a bank account?

The use is carried out and managed by the bank’s infrastructure.

Who controls access to cryptocurrencies?

Access is determined exclusively by the private key in your possession.

Can a bank prevent transactions?

Yes. The execution can be checked or suspended because it is carried out via a managed system.

Can a blockchain stop transactions?

No. However, without access to the key, no one can execute a transaction.

What happens if I lose access?

Access can usually be restored at banks, but this is generally not the case with blockchain systems.

Further reading

Ownership or Access? The Difference When It Comes to Money

Questions or personal classification

The issue of security in the financial system depends heavily on the underlying model. Traditional banks ensure security through institutions and regulation, while blockchain systems control access via cryptographic keys. Both approaches have different strengths and risks.

The key question, therefore, is: Which security model better aligns with your own sense of responsibility and control over your money?

If you’d like, we can take a quick look together at how the two systems differ and what role they can play in practice.

This page describes how payment systems work and does not constitute legal or financial advice.