To the overview of the basics

→ To the home page

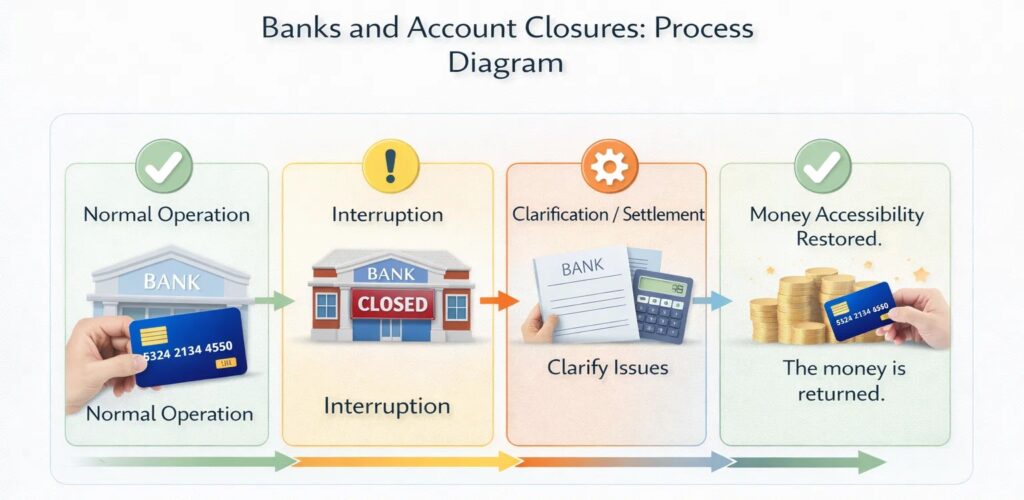

What happens when banks close or go bankrupt?

If a bank as an institution temporarily closes or is wound up, your money will not disappear — but access to it may be temporarily suspended until operations or the winding up have been settled.

This page explains what actually happens in such situations and why this depends less on the account balance than on the structure of the system.

This is hardly noticeable in everyday life because payment transactions are permanently available. It only becomes relevant when an institution’s operations are interrupted.

Table of Contents

What happens to your money

If a bank ceases operations or temporarily closes, nothing automatically happens to the balance itself. The account remains open, but access to it is technically suspended.

This means:

- Transfers are not being executed

- Cards are not functioning

- Payouts are not possible

The balance is still recorded, but cannot be used as long as the system is not working. The reason for this is that account balances represent a claim against the bank. As long as the institution is unable to operate, access cannot be provided.

During this period, we will determine how to continue or wind down operations.

You will retain your right to the balance, even if access is temporarily suspended.

Why banks can close at all

Banks are part of a regulated system. In certain situations, operations may be temporarily suspended, for example to organize processes or review assets.

Common reasons:

- technical or organizational disruptions

- liquidation proceedings

- Merger or transfer of institutions

- exceptional market conditions

A closure does not necessarily mean insolvency. Often, it is a planned suspension of operations to ensure that obligations can be properly settled. In many cases, efforts are made to transfer banking operations to another institution as quickly as possible.

In the event of insolvency, a security system kicks in, but only up to specified limits.

What works in the meantime — and what doesn’t

During this period, the difference between credit and access is particularly clear.

Not possible:

- withdraw money

- pay

- transfer

Still available:

- account balance

- legal claim

- later payment option

Many only notice the situation when a payment is no longer executed despite the money being available. It is precisely in such moments that it becomes clear that an account organizes access—it does not represent ownership itself.

How long restrictions may last

The duration does not depend on the account holder, but rather on when operations resume or responsibility is clarified.

This could be:

- a few days in case of technical interruption

- longer in terms of organizational processing

During this time, the credit balance remains unchanged, but access is paused.

When deposit protection applies

If a bank is finally wound up, statutory protection schemes come into effect. These protect deposits up to specified limits and ensure that claims for payment are retained.

In this case, the payout will not be made via the original account, but via the responsible security institution.

When this becomes relevant in everyday life

This difference is hardly relevant in normal payment transactions. It becomes apparent when availability can no longer be taken for granted.

Typical situations:

- Access becomes relevant when payments are tied to fixed dates and cannot be postponed.

- Access becomes relevant when multiple obligations run simultaneously through a single account.

- Access becomes relevant when an account is used as the sole source of liquidity.

In such moments, it becomes clear that an account organizes access—it does not represent immediate ownership. At this point, at the latest, it becomes clear that ownership and actual access are not the same thing.

Conclusion

A bank closure primarily affects access to funds, not their existence. The entitlement remains intact, even if use may be temporarily suspended. How noticeable this is in everyday life depends on how one’s own use is organized.

Such scenarios seem theoretical as long as they only affect others.

FAQ – Bank closure and payout

Will my money be lost if a bank closes?

No. The credit balance remains valid even if access is temporarily unavailable.

Wer zahlt mein Geld aus, wenn die Bank nicht mehr arbeitet?

Payment will be made either after operations resume or via the relevant security system.

How long will it take to get my money back?

That depends on the settlement procedure. Payment will be made as soon as the allocation of claims has been completed.

Do I have to apply for anything myself?

You will usually be informed about how the payment will be made and where it will be transferred to.

Can I access my account during this time?

No. During the suspension period, it is usually not possible to use the account.

Is this different from a normal account suspension?

Yes. This does not affect a single account, but rather the operation of the bank itself.

Further reading

Questions or personal classification

Solange ein Bankensystem stabil funktioniert, wird selten darüber nachgedacht, was passiert, wenn der Betrieb einer Bank unterbrochen wird. In solchen Situationen zeigt sich jedoch, wie der Zugriff auf Guthaben tatsächlich organisiert ist – und welche Rolle Sicherungssysteme, Abwicklungsverfahren und Infrastruktur dabei spielen.

Die entscheidende Frage ist deshalb: Was würde in deiner Situation passieren, wenn deine Bank plötzlich nicht mehr erreichbar wäre?

Wenn du möchtest, können wir kurz gemeinsam anschauen, wie solche Szenarien normalerweise ablaufen und welche Unterschiede zwischen verschiedenen Finanzsystemen bestehen.

This page describes how payment systems work and does not constitute legal or financial advice.