To the complete overview of the basics

→ To the home page

Can my bank freeze the account?

Yes, a bank can temporarily restrict access to your account or even freeze it entirely—even if the money legally belongs to you. The reason for this is that, technically speaking, a bank account isn’t a place where your money is stored, but rather access to a claim you have against the bank.

An account freeze imposed by the bank is different from government measures or official orders. In such cases, the bank makes the initial decision—usually based on internal audit requirements or legal regulations.

Classification

Many people associate account suspensions with fraud or criminal activity. In practice, however, they are often the result of automated verification processes:

The system assesses whether the use of an account fits the expected pattern.

This shifts the actual question:

Under what circumstances is a block triggered?

The question is therefore not: “Is your money still there?”,

but rather: “Can you use it right now?”

Table of Contents

What exactly is blocked when an account is suspended

An account freeze means that the bank temporarily deactivates access to your account, although the existing balance remains. The money is not removed or withdrawn. Only the functions that allow you to access your account are blocked. Many people only notice a freeze when a payment is declined despite having sufficient funds in their account.

Banks are legally obliged to carry out certain checks and may temporarily restrict access.

The background:

The balance in an account is not stored cash, but rather a claim against the bank.

As long as the system provides access, you can use this claim—for example, through transfers, card payments, or cash withdrawals.

During a suspension, this specific usage option is interrupted.

Typical effects:

- Transfers are not being executed

- Direct debits are rejected

- Card payments are declined

- Cash cannot be withdrawn

- Standing orders are paused automatically

The account still exists, but you no longer have access to it.

It is important to note the distinction:

An account freeze is neither a seizure nor a termination. The balance remains intact—only access to it is blocked.

For many, this only becomes apparent when everyday payments no longer work: rent, shopping, or gas station purchases are suddenly declined, even though there are sufficient funds available.

In short:

When your account is blocked, your money is still there—you just can’t use it temporarily.

Why banks are allowed to freeze accounts in the first place

Banks are permitted to freeze accounts because they are legally obligated to continuously monitor all account activity (e.g., requirements of the financial supervisory authority).

From the bank’s perspective, an account is not a neutral storage location, but part of a regulated payment system. The bank provides access and is liable for ensuring that no unauthorized or unclear money transfers take place.

This is subject to statutory audit requirements—for example, to prevent fraud, money laundering, or misuse. Today, these audits are largely automated: transactions are not evaluated individually, but are compared with expected usage patterns.

If usage deviates significantly from the usual profile, the system may restrict access as a precautionary measure until the matter has been clarified. The block is therefore not usually a punishment or a reproach. It is a technical security measure that enables the bank to fulfill its duty of verification.

Important to note:

Whether usage appears unusual depends less on the amount of money involved than on the recognizable pattern—in other words, how an account is typically used and what suddenly deviates from that pattern.

This often comes as a surprise to the account holder because the assessment is not based on intent, but on conspicuousness in the system.

In summary:

Banks do not primarily freeze accounts due to misconduct, but because they are legally obligated to temporarily review unusual usage patterns.

Which usage patterns can trigger a block

Account suspensions are rarely caused by individual amounts, but rather by deviations in an account’s usage pattern. Banks evaluate not only what is transferred, but above all whether the behavior matches the expected profile. If an account is suddenly used differently than before or than comparable accounts, an automatic check may be triggered.

Typical constellations are, for example:

Unusual individual transfers

An everyday account that is otherwise used regularly suddenly shows a significantly larger single transaction—for example, for a vehicle purchase, a private loan repayment, or a direct money transfer between private individuals.

Many incoming payments from different sources

Several small amounts from different senders within a short period of time can no longer be clearly assigned to a typical salary or private account by the system.

Use with foreign connection

Transfers from or to other countries, foreign currencies, or frequently changing locations alter the expected usage pattern of an account.

Prolonged inactivity followed by activity

An account is hardly used for a long time and then suddenly shows several transactions in a row or higher amounts than usual.

Transfer of funds

Incoming amounts are transferred in full or in part to other recipients shortly thereafter, without any discernible regularity such as rent or fixed bills. In all these cases, the system does not assess whether something is permitted or prohibited. It merely recognizes that the use can no longer be clearly assigned and therefore needs to be checked. This often comes as a surprise to the account holder, because each individual payment appears plausible when viewed on its own — but the pattern as a whole no longer corresponds to the expected behavior.

In summary:

It is not the amount that determines whether an account may be blocked, but whether the use is still recognizable as normal for the system.

If access can be restricted, the next question inevitably arises:

What actually happens if not just individual accounts, but the bank itself fails?

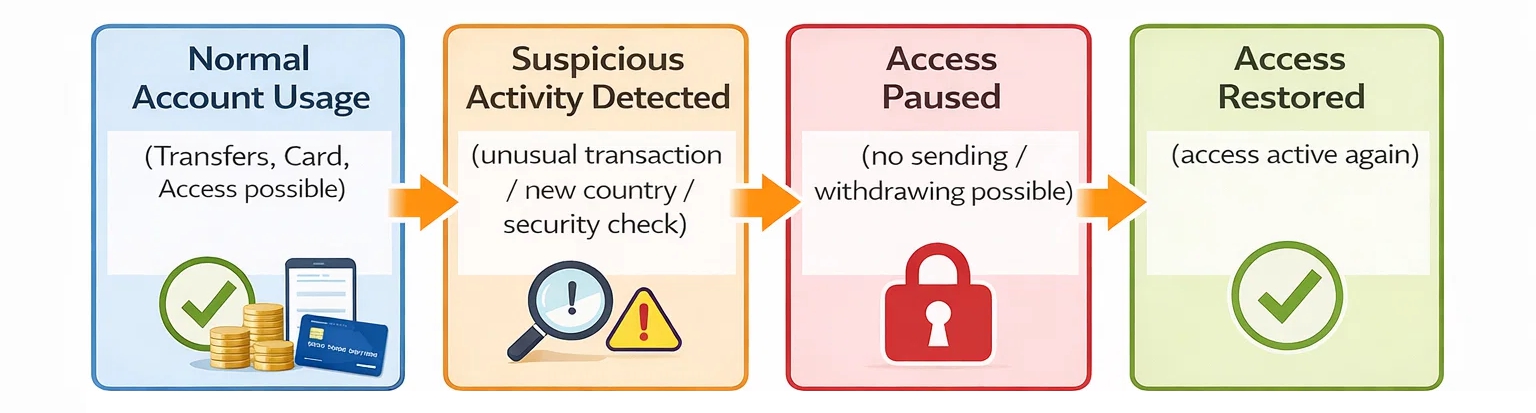

How account suspension works in practice

An account freeze usually happens without warning and only becomes apparent when the account is used. Access is technically restricted as soon as a verification process is initiated. For the account holder, this usually first becomes apparent when a payment is no longer executed.

Typical procedure:

- A bank transfer or card payment is declined

- Online banking is functioning with restrictions or not at all

- Standing orders or direct debits are not executed

- Only then will you receive a message from the bank or a query.

At this point, the lock is often already active.

The bank then requests documentation or an explanation regarding the specific transaction—such as the origin of an amount, the purpose of a payment, or the relationship to the recipient. Access remains restricted during this clarification process.

Important:

The check does not only refer to the individual transaction, but to its classification in the entire account history.

This is why blocks often cannot be lifted immediately by telephone.

For those affected, the situation usually arises unexpectedly in everyday life—when paying in a store, making a bank transfer, or when a regular payment is suddenly returned.

In summary:

An account block is usually only noticed when a payment fails — clarification begins after that, not before.

How long you cannot access your money

The duration of an account freeze is not fixed. It only ends once the bank has been able to sufficiently clarify the underlying circumstances.

In simple cases, this can happen within a few days—for example, if the requested documents are immediately available and can be clearly assigned. However, the review often takes longer because several transactions have to be examined or information from third parties has to be taken into account. During this time, access remains restricted, even if the credit balance is still available.

Typical periods may be:

- a few days for clearly traceable payments

- several weeks for more complex processes or international involvement

- longer if information is missing or questions remain unanswered

The decisive factor here is not so much the amount as the traceability of the use. As long as the system cannot clearly classify a transaction, the block remains in place.

For the account holder, this means in practical terms:

Ongoing obligations such as rent, bills, or everyday payments cannot be processed via this account during this period.

In summary:

An account suspension lasts until the use has been fully clarified — not until a fixed date.

In which situations this also affects normal users

Accounts are not only blocked in cases of unusually high amounts or clearly problematic transactions. They often relate to everyday usage situations that seem normal to the account holder but do not form a clear pattern in the system. The decisive factor here is not the individual payment, but the combination of several characteristics: the origin, frequency, and context of the transactions.

Certain usage patterns occur particularly frequently:

Revenue from various sources

A block may occur if, in addition to a salary, additional amounts are received from various sources—such as sales, private repayments, investments, or project-related income. Each individual payment is traceable, but together they do not form a clear account profile.

Transferred or jointly managed funds

A block may occur if amounts received are transferred in whole or in part to other persons—for example, collective payments or joint expenses. This is logical for the user, but difficult for the system to assign.

Use across national borders

A block may occur if payments are made across countries or from changing locations. The use no longer clearly corresponds to a local everyday account.

Irregular major purchases

A block may occur if higher individual amounts suddenly appear on an otherwise inactive account—for example, for vehicles, down payments, or private agreements between individuals.

Alternating between prolonged rest and activity

A block may occur if an account that has hardly been used for a long time suddenly shows several transactions in a short period of time. In such situations, there is no misconduct. However, the system cannot clearly classify the use and stops access until the assignment has been clarified.

Whether this actually results in a restriction does not depend on the user’s intention, but on how clearly the use can be interpreted automatically. Many only realize afterwards that their everyday use does not correspond to the expected standard profile.

In summary:

It is not specific actions that typically lead to an account being blocked, but rather usage that cannot be clearly classified by a system.

What you can do during a lockout — and what you can’t

If an account has been restricted, the situation usually cannot be expedited by immediate inquiry or repeated contact. Approval will only be granted once the requested classification has been provided in full.

It is therefore particularly helpful to respond to the bank’s inquiry in a structured manner.

Meaningful steps:

- submit all requested documents

- clearly describe the purpose of the payment in question

- Explain the relationships between multiple transactions

- Respond to inquiries instead of initiating new transfers

On the other hand, it is less helpful:

- calling repeatedly without providing any new information

- Try payments again in parallel via the same account

- Splitting amounts to circumvent the original transaction

Since the audit considers not only individual payments but the entire context, additional unclear movements often prolong the clarification process.

In practical terms, this means that during the restriction period:

Ongoing expenses must be paid using other available payment methods until access is restored.

In summary:

An account suspension cannot be expedited — it ends when the usage can be clearly classified.

If access can be restricted, the next question inevitably arises: What actually happens if not just individual accounts, but an entire bank fails?

Conclusion

In most cases, account suspension is not an unusual event, but rather the result of usage that cannot be clearly interpreted by an automated system.

Whether an account will ever be restricted cannot therefore be determined solely on the basis of the account balance or individual payments. The decisive factor is whether the overall usage corresponds to a clearly recognizable pattern.

While many accounts remain permanently inconspicuous, restrictions typically arise where usage and classification diverge. Some constellations can be explained in general terms—others depend on the individual usage situation.

If you are unsure how a particular use will be assessed structurally, you can write to me about it.

Account access seems like a given—until it is interrupted.

FAQ – Account suspension and ownership

-

Can a bank temporarily restrict my account?

Yes. Banks may temporarily suspend access if transactions need to be verified or allocated.

-

Why is my account being verified even though I have money in it?

Because it is not the account balance that is evaluated, but rather the classification of individual payments within the system.

-

How long does an account suspension usually last?

The duration depends on when the usage can be clearly assigned and the review is complete.

-

Can I receive money during this time?

In many cases, yes, but usage may remain restricted until the review is complete.

-

Will my account be automatically reactivated afterwards?

As soon as the usage can be classified, access will be restored.

-

Does this only happen with unusually high amounts?

No. The decisive factor is not the amount, but whether the use is clearly traceable.

Further reading

- Can the government freeze my account? EU rules, reasons, and consequences

- What happens to my money if a bank closes?

- Ownership or access? The difference explained simply

- Crypto or bank—which is safer?

Questions or personal classification

Account freezes come as a surprise to many people because, in everyday life, an account seems like a personal place to keep money. In practice, however, banks manage the infrastructure through which payments are processed. As a result, audits, security protocols, or legal requirements can lead to temporary restrictions on access to an account.

The key question, then, is: To what extent does your ability to access your own money actually depend on your bank?

If you’d like, we can take a quick look together at how such situations can arise and what role different banking structures play in them.

This page describes how payment systems work and does not constitute legal or financial advice.