To the overview of the basics

→ To the home page

Who really owns the money in a bank account?

In everyday life, having a bank balance feels like you simply own your money.

You see your balance and can make transfers, pay bills, or withdraw cash.

Legally, however, a bank account works a little differently. The balance does not belong directly to you; rather, it represents a claim against the bank. So you do not own the deposited amount of money; you merely have the right to use it.

So the real question is: “Who decides when you can use it?” Whether you can actually use it depends on how access is organized. On this page, we’ll take a closer look at what that means in practice.

Table of contents

Why this is so

In everyday life, an account feels like a personal storage space. In fact, it works differently from a technical standpoint.

When money is deposited into an account, the following happens in simplified terms:

- The cash becomes the property of the bank.

- The bank will credit your account for this.

- This credit balance is a promise to pay.

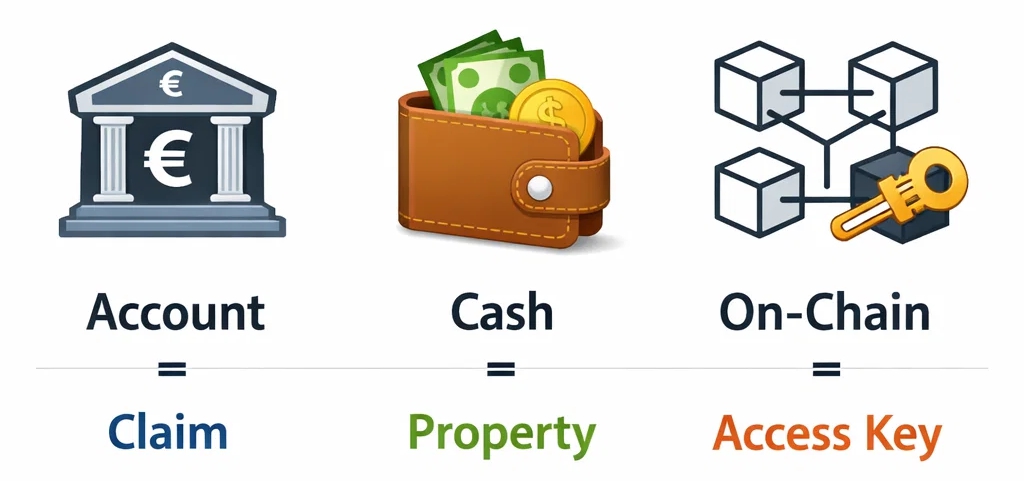

So you don’t actually own the money in your account. Instead, you simply have a claim that the bank will pay you that amount at any time.

As long as the processes run automatically, this difference seems insignificant. It is only when payments are reviewed, delayed, or restricted that it becomes clear how access is actually organized.

The difference between ownership and access

This is where the most common misunderstanding arises.

Possession

- direct control over money

- system-independent

Access

- Permission to use the money

- depending on the infrastructure

A bank account provides access, but not immediate ownership. This works fine in everyday life as long as everything runs normally.

As long as payments work automatically, this difference seems unimportant. It only becomes apparent when a decision has to be made as to whether a transaction should be executed or checked.

When this difference becomes apparent

The difference is that access is provided technically and is not directly related to the money itself, e.g. in the case of:

- Account checks

- security checks

- technical limitations

- regulatory requirements

- System malfunctions

In these situations, it is not the account holder alone who decides, but the institution that manages access.

This does not mean that banks “act arbitrarily,” but rather that the system is designed precisely this way. In such moments, it becomes clear in practice that access is a provided function — not immediate ownership.

Why the banking system is structured this way

The traditional banking model is based on money being managed centrally.

This enables:

- Bank transfers

- Card payments

- lending

- Liquidity in the economic system

For this to work, the bank must have legal access to the deposited money. That is why deposited money becomes a claim.

Modern digital systems

New financial structures attempt to organize this point differently: not via institutional access permissions, but via technically defined access rules.

The goal is not to completely replace banks, but to diversify access and control. Some systems today combine both approaches: traditional payment functions and direct access control.

Why this question is important

This difference is hardly relevant in everyday life. It becomes relevant when considering the question:

Who ultimately decides on the availability of money?

The answer does not depend on the account balance, but on the structure through which the money is managed. This means that availability does not depend on the location of the money, but on how access is provided.

When this becomes relevant in everyday life

The difference between ownership and access is not apparent during normal operation. It only becomes apparent in situations where a system classifies or verifies usage, for example when:

- Payments will be verified.

- involves multiple systems.

- Accounts may be temporarily restricted.

- Processes do not run automatically.

In such cases, it is not the account holder who decides how the account is used, but the system that provides access.

At this point, at the very latest, a simple question arises:

Even if you own the claim—can you dispose of it at any time?

Many people only start thinking about this issue when something in the system stops working as expected. Others look into the options available today for organizing access to and control over their money in a more independent way.

Conclusion

A bank account is not a safe deposit box, but an agreement.

You do not own any deposited money; rather, you have a claim to it, entitling you to use it at any time. As long as systems function smoothly, this distinction makes little difference in everyday life. It only becomes relevant at the moment a decision is made about whether or not to make a transaction. That is when it becomes clear how money is actually organized.

The question of who legally owns money seems abstract—until you apply it to your own account.

How would you access your money if your bank were temporarily unavailable?The question of who legally owns money seems abstract—until you apply it to your own account.

How would you access your money if your bank were temporarily unavailable?

FAQ – Frequently asked questions about account balances

Does the money in my bank account belong to me?

No. Legally, the money you deposit belongs to the bank. Instead, you have a claim against the bank to have the amount paid out at any time.

Can I always freely access my account balance?

Not arbitrarily, but it can temporarily restrict access, e.g., during audits, technical problems, or legal requirements. During this time, your claim remains valid, but access is blocked.

Is cash legally different from account balances?

Yes. Cash is your immediate property. Account balances, on the other hand, are claims for payment against an institution.

What happens to my credit balance if a bank becomes insolvent?

Your credit balance remains a claim in the insolvency proceedings. Depending on the security system, part of it may be secured, but access is not immediate.

Why is money organized as a claim in the first place?

This is the only way the bank can technically process transfers, card payments, and loans. The system is based on money being managed centrally.

Further reading

The following topics build on this:

- Can the bank freeze my account? – Reasons and consequences

- Can the government freeze my account? EU rules, AMLA, DAC8, CARF, and what this means in practice

- What happens to my money if a bank closes?

- Ownership or access? The difference when it comes to money

- Crypto or bank—which is safer?

Questions or personal classification

Many people are surprised to learn that the money in a bank account does not legally belong to them directly, but rather constitutes a claim against the bank.

This page explains the underlying structure. However, how this affects control and access in practice always depends on the specific situation.

The key question, therefore, is: How would you access your money if you suddenly needed to withdraw all of it today?

If you’d like, we can briefly go over this. There’s no obligation involved—it’s just a quick assessment of your situation.

This page describes how payment systems work and does not constitute legal or financial advice.